Newsletter – 4/22/2024

Week of April 15, 2024 in Review

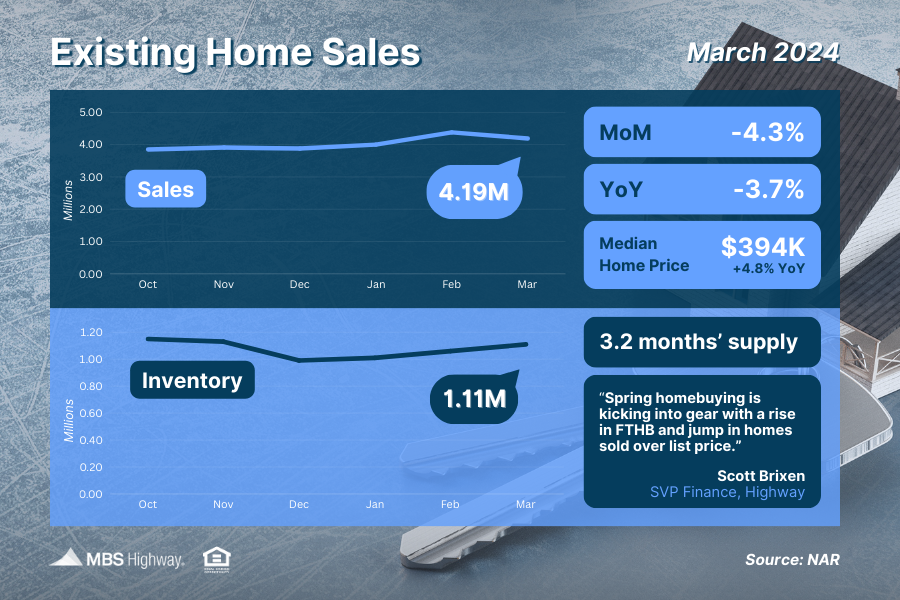

Existing Home Sales Slip

After hitting their highest level in a year in February, Existing Home Sales fell 4.3% in

March to a 4.19-million-unit annualized pace, per the National Association of

REALTORS (NAR). This report measures closings on existing homes in March and

likely reflects people shopping for homes in January and also in February when rates

began to tick higher.

What’s the bottom line? While the pace of sales declined in March, it remains at the

second highest level since last May, with NAR’s Chief Economist, Lawrence Yun,

confirming that sales have rebounded from cyclical lows.

In addition, some of the internals within the report showed signs of strength. Homes

remained on the market for a shorter period (an average of 33 days in March down from

38 days in February), while a greater number of homes sold above list price (29% in

March versus 20% in February). This signals demand and competition remains ahead

of the spring buying season.

Plus, there was some good news on the inventory front, as there were 1.11 million

homes available for sale at the end of March, up 4.7% from February and 14.4% from a

year earlier. While this remains below healthy levels, rising inventory is certainly a step

in the right direction to help improve the persistent tight housing supply we’ve seen

across the country. Yun added that “more inventory is always welcomed in the current

environment.”

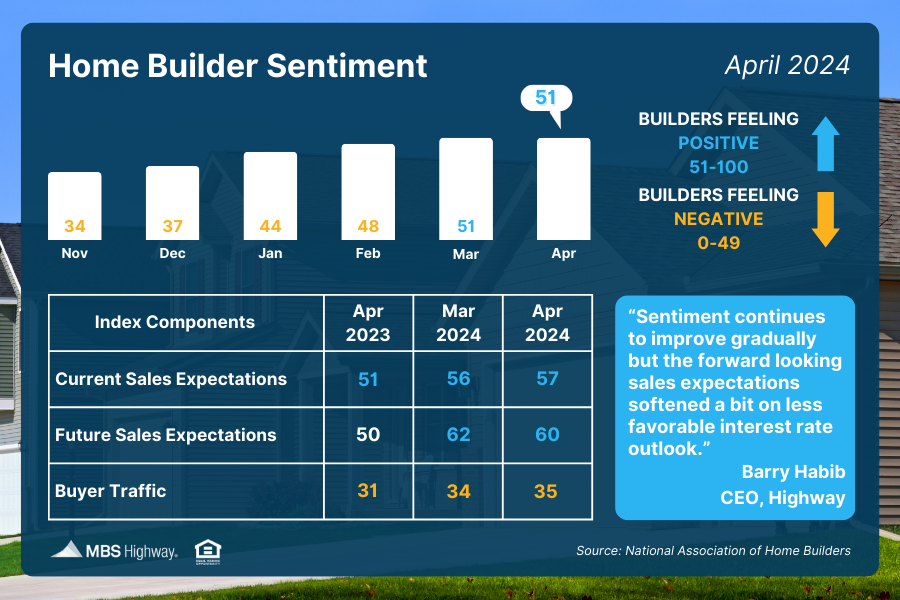

Home Builder Sentiment Holds Steady

Confidence among home builders remained just above the key breakeven threshold of

50 for the second straight month, per the National Association of Home Builders

(NAHB), as their Housing Market Index stayed at 51 in April. Any score over 50 on this

index, which runs from 0 to 100, signals that more builders view conditions as good than

poor.

Among the three index components, current and future sales expectations both remain

in expansion territory at 57 and 60, respectively, though future expectations have

softened as some buyers remain on the fence. The gauge judging buyer traffic moved

higher, but it’s still in contraction territory.

softened as some buyers remain on the fence. The gauge judging buyer traffic moved

higher, but it’s still in contraction territory.

What’s the bottom line? NAHB’s Chief Economist, Robert Dietz, explained, “April’s flat

reading suggests potential for demand growth is there, but buyers are hesitating until

they can better gauge where interest rates are headed.”

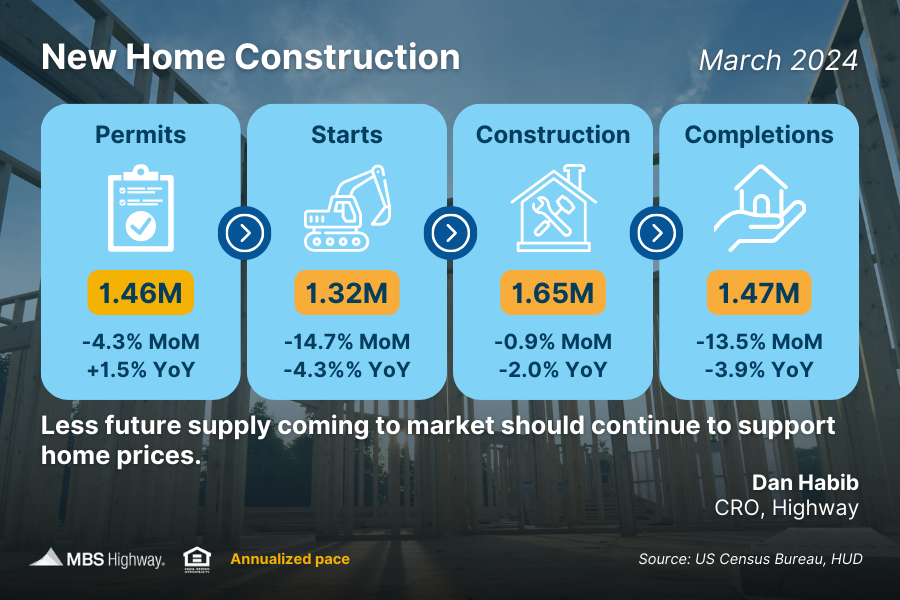

Housing Starts Slide in March

Even though home builder sentiment held steady, builders pulled back on new

construction last month, with Housing Starts falling nearly 15% from February. Starts for

single-family homes, which make up the bulk of homebuilding and are the most crucial

due to buyer demand, were also down 12.4%. There was a similar trend in future

construction, with Building Permits moving lower despite much needed supply.

What’s the bottom line? The NAHB noted that higher than expected interest rates,

hotter than anticipated inflation, and higher supply side costs all contributed to the

construction slowdown last month. Danushka Nanayakkara-Skillington, NAHB’s

Assistant VP for Forecasting and Analysis, added that single-family construction will

also likely decline in April, given the drop in building permits last month.

Home prices should remain supported, as there still is not enough supply coming on the

market to meet demand, showing that opportunities remain to build wealth through

homeownership.

Rates Higher for Longer

While speaking to a policy forum on U.S.-Canada economic relations, Fed Chair

Jerome Powell said that recent data has “clearly not given us greater confidence” that

inflation is moving toward the Fed’s 2% target. This includes hotter than expected

consumer inflation readings in recent months, especially as measured by the Consumer

Price Index.

Remember, the Fed aggressively hiked their benchmark Fed Funds Rate (the overnight

borrowing rate for banks) eleven times between March 2022 and July 2023 to slow the

economy and curb runaway inflation. The Fed has held rates steady as of their meeting

last September because inflation had been showing good progress lower before stalling

in more recent reports.

What’s the bottom line? Powell said it will likely take longer to achieve confidence that

inflation is progressing lower, signaling that the timing for rate cuts will probably be

delayed and rates will be higher for longer until confidence is restored. This more

hawkish tone was echoed by other Fed members last week as well, including New York

Fed President John Williams and Atlanta Fed President Raphael Bostic.