Week of April 22, 2024 in Review

Inflation Progress Getting Harder:

March’s Personal Consumption Expenditures (PCE) showed that headline inflation rose

0.3% from February, with the year-over-year reading up from 2.5% to 2.7%. Core PCE,

the Fed’s preferred method which strips out volatile food and energy prices, also rose

by 0.3% monthly. The year-over-year reading held steady at 2.8%, stalling progress

toward the Fed’s 2% target.

What’s the bottom line? The Fed has been working hard to tame inflation, hiking its

benchmark Fed Funds Rate (which is the overnight borrowing rate for banks) eleven

times between March 2022 and July 2023. These hikes were designed to slow the

economy by making borrowing more expensive, lowering the demand for goods, and

thereby reducing pricing pressure and inflation.

The Fed has held rates steady since last September because inflation had been

showing good progress lower before stalling in more recent reports. At their meeting in

March, the Fed still signaled that three rate cuts are ahead this year. Will they change

their tune at their meeting this week? We’ll find out on Wednesday with their Monetary

Policy Statement and press conference.

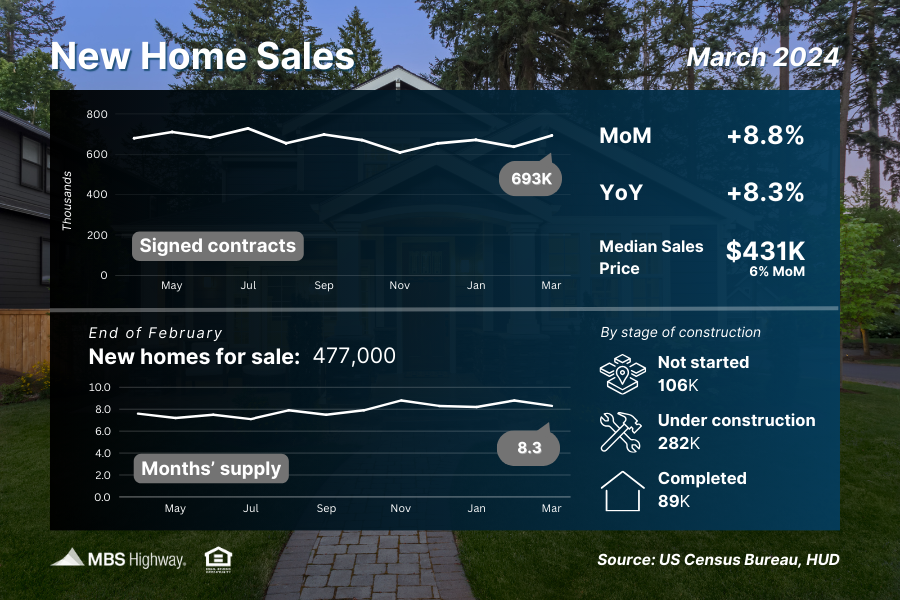

New Home Sales Data Confuses Media

After falling in February, signed contracts on new homes rebounded 8.8% in March to a

693,000-unit annualized pace, reaching their highest level since September. Sales were

also 8.3% higher than a year earlier, as the persistent shortage of previously owned

homes for sale continues to fuel demand for new construction.

What’s the bottom line? Despite the strong headline figure, some media pundits

pointed to the decline in the median sales price, which was down nearly 2% from a year

ago, to say the report was a miss. But the median sales price did not decline because of

falling home prices (which continue to rise per Case-Shiller and other indexes), or a

growing number of price cuts from builders. In fact, 36% of builders reported cutting

prices in December, versus just 24% in March and 22% in April per the National

Association of Home Builders.

The median sales price represents the mid-price of sales, meaning it’s influenced by the

mix of sales in any given month. March’s decline in the median sales price stems from

the sale of more homes at lower price points. Builders are constructing smaller, more

affordable homes to meet buyer demand, and that pushed the median sales price lower

comparatively.

Signed Contracts on Existing Homes March Higher

Pending Home Sales rose 3.4% from February to March per the National Association of

REALTORS (NAR), coming in well above estimates. This report measures signed

contracts on existing homes, making it an important forward-looking indicator for

closings on these homes, which are measured in the Existing Home Sales report.

What’s the bottom line? The Pending Home Sales index hit its highest level in a year,

showing that activity is picking up heading into the spring homebuying season. An

increase in inventory and eventual decline in mortgage rates will only boost these sales

figures, with NAR’s Chief Economist, Lawrence Yun, noting, “Inventory will grow

steadily from more home construction, and various life-changing events will require

people to trade up, trade down or move to another location.”

First Quarter GDP Weaker Than Expected

The first reading of first quarter 2024 Gross Domestic Product (GDP) showed that the

U.S. economy grew by 1.6%. This was well below both the 2.5% estimate and the 3.4%

growth seen in the fourth quarter of last year.

What’s the bottom line? Slower economic growth is typically good news for the bond

market, but the hotter than expected inflation component within the report led to a sell-

off when the data was reported last Thursday. Note that this data is subject to revision

when the second and final readings are released on May 30 and June 27, respectively.

However, the weaker than expected initial reading is disappointing given that GDP

functions as a scorecard for the country’s economic health.

Initial Jobless Claims Hit 9-Week Low

Initial Jobless Claims fell by 5,000 in the latest week, as another 207,000 people filed

for unemployment benefits for the first time. Continuing Claims also declined by 15,000,

with 1.781 million people still receiving benefits after filing their initial claim.

What’s the bottom line? The low level of Initial Jobless Claims suggests that

employers are still trying to hold on to their workers. Yet, Continuing Claims are still

trending near some of the hottest levels we’ve seen in recent years, as challenges

remain for job seekers searching for their next position.

What to Look for This Week

Housing and labor sector data will share headlines with the Fed, starting Tuesday with

appreciation data for February from Case-Shiller and the Federal Housing Finance

Agency. We’ll also see updates on job openings and private payrolls (Wednesday),

unemployment claims (Thursday), and nonfarm payrolls and the unemployment rate

(Friday).

The Fed’s meeting begins Tuesday, with their Monetary Policy Statement and press

conference coming on Wednesday. Investors will be closely listening for news regarding

the timing of rate cuts later this year.

Technical Picture

Mortgage Bonds continue to trade in a wide range between support at 98.867 and

overhead resistance at 99.647. The 10-year retreated from the yearly high it reached

last Thursday, and there is room for yields to improve and move lower if we receive

some Bond-friendly news this week.